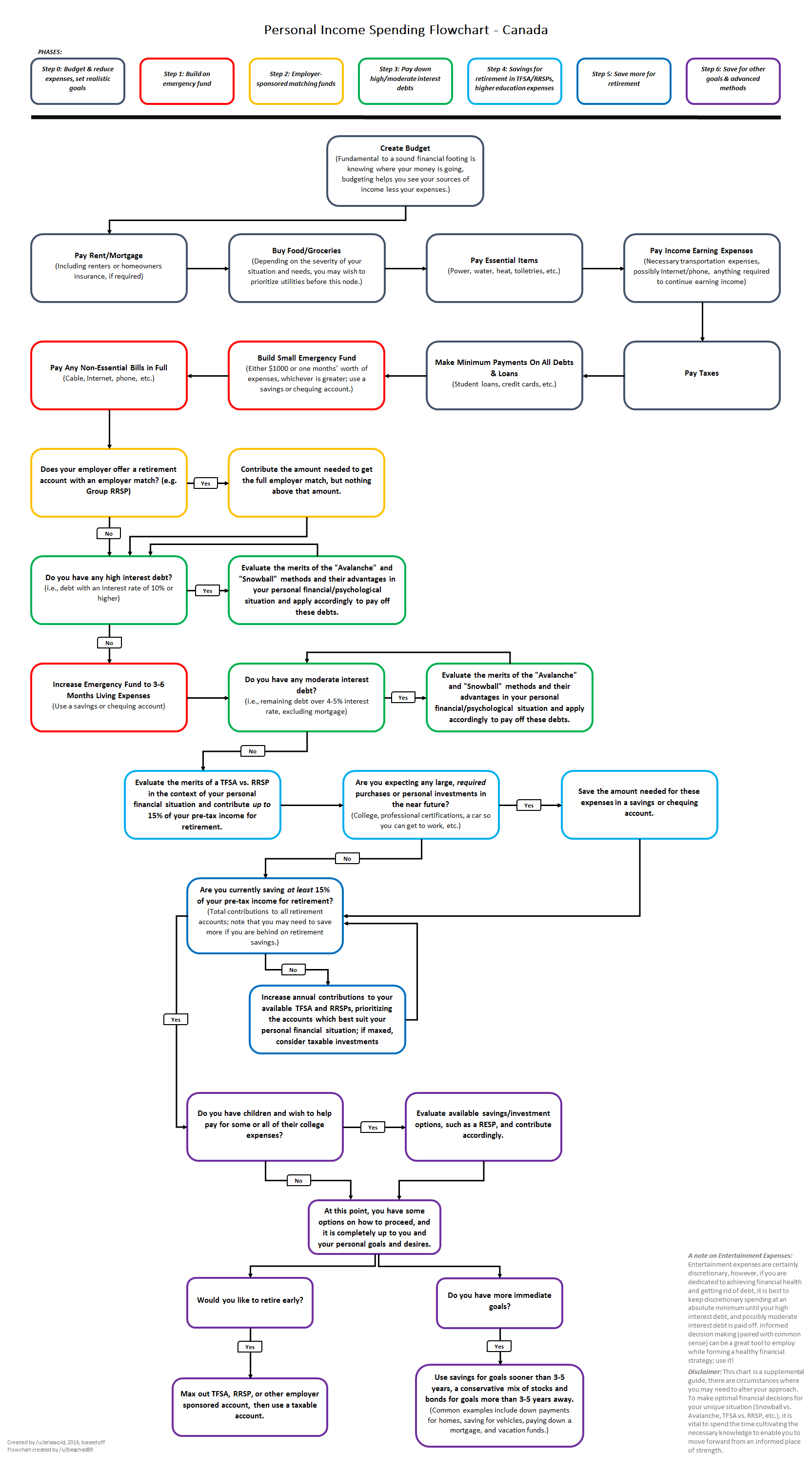

In an effort to get more activity in this community, I'd like to start a discussion on how you evaluate which insurance plans to choose. Now, it is much simpler to do so when none of the plans you're offered have HSA. With HSA plans and employer HSA contributions I found it's actually quiet difficult to do all the math to figure out which plan will get you the most bang for your buck. The biggest thing you have to take into account is your expected annual healthcare expenses. Once you start taking into account things like pre-tax cost (premiums, HSA contributions) vs post-tax costs (your out of pocket post-tax expenses), your tax rate etc, you can get deep into a rabbit hole and find some surprising results.

I'm actually working on an Excel spreadsheet that allows me to compare up to 4 plans and tells me which plan is the most cost effective, depending on my annual expected OOP healthcare expenses. You input things like annual plan premiums, HSA employer contributions (if any), your HSA contributions (if any), plan's out-of-pocket maximum (per person), plans out-of-pocket maximum (per family) and your tax bracket and the spreadsheet will spit out a chart telling you the relationship between your expected OOP annual expenses and the true cost you have to incur if you choose this plan. What surprised me the most is that the high deductible/high OOP-maximum HSA plan is actually the best/the most cost effective plan in basically any situation, especially if I max out my HSA contributions (this may not be true in your case, you have to run the numbers yourself). The reason for this is that while the regular PPO plans have lower OOP max, I would pay a lot more in premiums for them, which is a hidden cost a lot of people don't consider. Also, the OOP expenses in PPO plans are all post-tax, while I get to pay my OOP expenses with pre-tax dollars if I choose an HSA plan, which matters a lot.

If anyone is interested, I'd be happy to share my spreadsheet to test it more and make sure I'm not missing anything important. Feel free to share your strategy as well if you recently had to make a choice between several plans, what plan you chose and what guided you to that decision.